Several factors affect the value of a house, and a single house may be valued at varying figures.

Several factors affect the value of a house, and a single house may be valued at varying figures.

The two assessments of primary concern to buyers and sellers are the market value and the appraised value but other factors such as appraised also comes into play. Understanding a home’s true market value is about more than pictures, software assessments and price-per-square-foot. Whether you’re a current homeowner thinking of selling or are house-hunting, it’s crucial you understand what factors affect home valuation. By partnering with a local market expert, sellers will avoid pricing their house out of the market (the kiss of death in real estate) and buyers will ensure they get a good deal on their next home.

The market value of a home is determined by what buyers will pay for that one house and other similar homes in the neighborhood. The specific features of home, such as hardwood flooring and triple pane windows do influence how a real estate agent may price a home, but the pricing is primarily based on "comps". "Comps" is a real estate term for a list of homes in the area comparable to the house being priced that sold within the last few months. The agent looks at the final selling prices of these homes and uses them to fix a price to a specific house.

The factors that influenced those final selling prices include location, condition of the property, appeal of specific features such as the floor plan and size of the bathrooms, and sellers’ terms. This last item refers to whether the seller will pay closing costs or provides a warranty on the home. Putting all these factors together and referencing them to the house being priced, the agent then makes an assessment that is aligned with the recent sales. The most important factor, though, remains the final selling price: What are buyers willing to pay for a home in a specific neighborhood with these features. That price is market value.

An appraised value depends on location and condition of the home, and to some extent the features of the home. A buyer is concerned with the appraised value because it is that figure the bank will rely upon to determine if the home is a sound investment and whether or not the buyers can obtain a mortgage. When buyers apply for a mortgage on a house, the bank may send out an appraiser to the property. The appraiser then assesses the value of the home based on the condition of such structural elements as heating and cooling systems, plumbing and electrical and the condition of the foundation. He or she will also assess the overall condition of the home, from flooring to bathroom fixtures to the type of windows in the house. The appraised value of the home is based on the age and overall condition of the home, the type of materials and goods used in the construction of the home, and the stability of the neighborhood in regard to market value.

While market value does factor into an appraisal, its influence is only as an indication of the consistency of neighborhood’s economic stability. Lenders do not want to invest in an unstable area in which the market value differs from year to year. If the two assessments, the market value and the appraised value are not too far apart the buyers will get their loan. If the appraised value is considerably below market value, in terms of several thousand dollars, the buyers are unlikely to get a loan using that house as collateral.

So, how do you accurately calculate a home’s value? After all, the value a home is assigned by its town or county and the one it’s given when it’s listed are often dramatically different from one another. Which one is accurate and what does it all mean? Read on to learn more.

Assessed Value vs Market Value: What’s the difference?

When it comes to home value, you’ll often hear two terms, assessed value and market value.

A home’s assessed value is often the lower number of the two and is the value given by your municipality or county. Investopedia defines assessed value as “the dollar value assigned to a property to measure applicable taxes.”. Although property tax laws vary, assessors commonly arrive at this number by taking into account the following:

- What comparable/similar homes are selling for in your area.

- The value of recent improvements.

- Income from renting out a room or space on the property.

- How much it would cost to rebuild on the property.

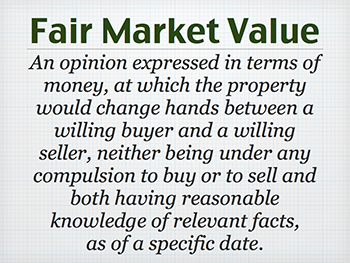

A home’s market value, or Fair Market Value, is the price a buyer is willing to pay or a seller is willing to accept for a property. A skilled real estate professional will arrive at the value using a variety of metrics, including:

A home’s market value, or Fair Market Value, is the price a buyer is willing to pay or a seller is willing to accept for a property. A skilled real estate professional will arrive at the value using a variety of metrics, including:

- External characteristics, such as lot size, home style, the condition of the home and curb appeal.

- Internal characteristics, such as the number of rooms and their size, the type and condition of the heating or HVAC system, the quality and condition of construction, the flow of the home, etc.

- The sales price of comparable homes that have sold in your area.

- Supply and demand; that is, how many buyers and sellers are in the area.

- Location; that is, the quality and desirability of your neighbourhood and other community amenities.

Why are these values often so different? An assessor usually estimates your property’s market value during a reassessment or if you make a physical change or improvement to it. As a result, a property may not be reassessed for many years. While your home’s market value may fluctuate with the market, your home's assessed value is more likely to remain steady.

What does the government of BC say?

Your property assessment significantly influences the amount of property taxes you pay. You will receive your property assessment notice from BC Assessment each year in January. Your property is assessed to determine its Value, Classification and Exemptions (if any apply).

In most cases, the value is an estimate of your property's value as of July 1 of the previous year. To determine the value of your property, an assessor compares your property to actual sales in the same area. Some of the characteristics the assessor compares are:

- Location

- Size

- Land surface (topography)

- Shape

- Use

- Age and condition of buildings

If you notice an issue or have a question about your property assessment, contact BC Assessment to discuss your concerns. If your concerns are not resolved, an independent appeal process exists to have your assessment reviewed. The first level of appeal is to the Property Assessment Review Panel (PARP). If you appeal, once a decision is made your property taxes may change; this change may result in a tax decrease (you may qualify for a refund if you paid a higher amount of property taxes) or a tax increase (you will pay a higher amount of property taxes)

What Determines a Kamloops Home’s Value?

You’ve likely heard the motto of real estate: “Location, location, location.” This means a home’s value relies on its location. While the home and structures on the property will likely depreciate over time, the land beneath it tends to appreciate. Why? Land is in limited supply and a growing population puts increased demand on the housing supply, as a result, values increase.

You’ve likely heard the motto of real estate: “Location, location, location.” This means a home’s value relies on its location. While the home and structures on the property will likely depreciate over time, the land beneath it tends to appreciate. Why? Land is in limited supply and a growing population puts increased demand on the housing supply, as a result, values increase.

Other factors that affect your home’s value include the function and appearance of the property, how well the home and other structures are maintained and whether the home is a lifestyle property, such as a ranch style with mountain views or beach bungalow.

Ultimately, the best indication of a home’s value is the overall supply and demand of the market. This is why we recommend you partner with a real estate professional who takes all of these factors—the assessed value, local market conditions, home features and has physically walked through and experienced your home— into consideration to determine the most accurate market value.

How to determine if a property is comparable to yours.

Both assessed value and market value are partially determined by the sales price of similar, or comparable, homes in the area. To determine if a home is comparable to yours, look for the following characteristics:

- Lot size

- Square footage

- Homestyle or similar architecture

- Age

- Location

While you may not find a home with the same exact characteristics as yours, you’ll likely find a few that are close. To account for any disparity, adjust the sales prices of the comparable properties. Look at the differences between your property and the one in question and determine if the differences increased or decreased the sales price and by how much. For example, if your home has two bathrooms and a similar home only has three, estimate how much that extra bathroom increased the sale price of a similar home. The adjusted sale price is the estimation of what the property would sell for if the properties were exactly the same.

Where can you find comparable sales?

Fortunately, you can find comparable home sales in a variety of places.

- Your local assessor’s office is able to provide a list of recent sales you can browse and compare or a sales history of a particular house, home style or neighbourhood.

- Your municipality. Many cities keep local sales information in their offices or post it online.

- Online databases, such as a real estate database

- Your local newspapers may offer some real estate information in the form of quarterly sales reports in the business or real estate sections of the newspaper.

- My office. I regularly do Comparable Market Analysis of homes in our local area.

How to calculate your Kamloops home’s value.

By answering a few questions about your home, property and the local market, you can begin to estimate your property’s value. We’ve also included a worksheet for you below...

Home Value Questions:

- When was your home last assessed?

- What was its CMA assessment value?

- What is your area’s average sales price?

- What is your area’s average price/square foot?

Structure:

Structure:

- Are the architecture and exterior structure of the home consistent, superior or inferior to other homes in the area?

- Does the era or genre (Modern, Victorian, Ranch, Cottage, etc.) add a premium based on current design trends?

- How does the floor plan and room size proportions of the home compare to other homes on the market?

Interior Structure:

- How does the kitchen compare to others on the market?

- Updated or outdated

- Floorplan

- Appliance packages

- How does the Master Suite compare to others on the market?

- Size

- First/second floor

- Updated or outdated

- Access to Master Bath

- How does the Master Bath compare to others on the market?

- Updated or outdated

- Shower and bath

- Flooring

Outside Areas:

- Are there views, outdoor living areas or recreational areas?

- Pools

- Ponds

- Patios

- How does the landscaping and hard-scaping compare to the market? (e.g., built elements such as walkways, patios, decks, etc.)

- Overall Condition of HomeWhat is the level of repair needed to compete with other homes?

- Does the home need to be staged? How does it show?

- What curb appeal projects are necessary to be consistent with others on the market

If you want to accurately assess a home’s value, it’s crucial to know about the market activity of our local area. I can help! Give me a call to get the scoop on the local market. (250).319.5896